Graphic:

Excerpt:

The concern with this exercise is its reliance on past returns. With interest rates near zero, significant economic growth is needed to generate market returns close to those experienced over the last 100 years – approximately 11% per annum. To explore the implications of different future investment performance, let’s repeat the process above by reducing the average return of historical stock returns while maintaining the same risk (i.e., volatility).

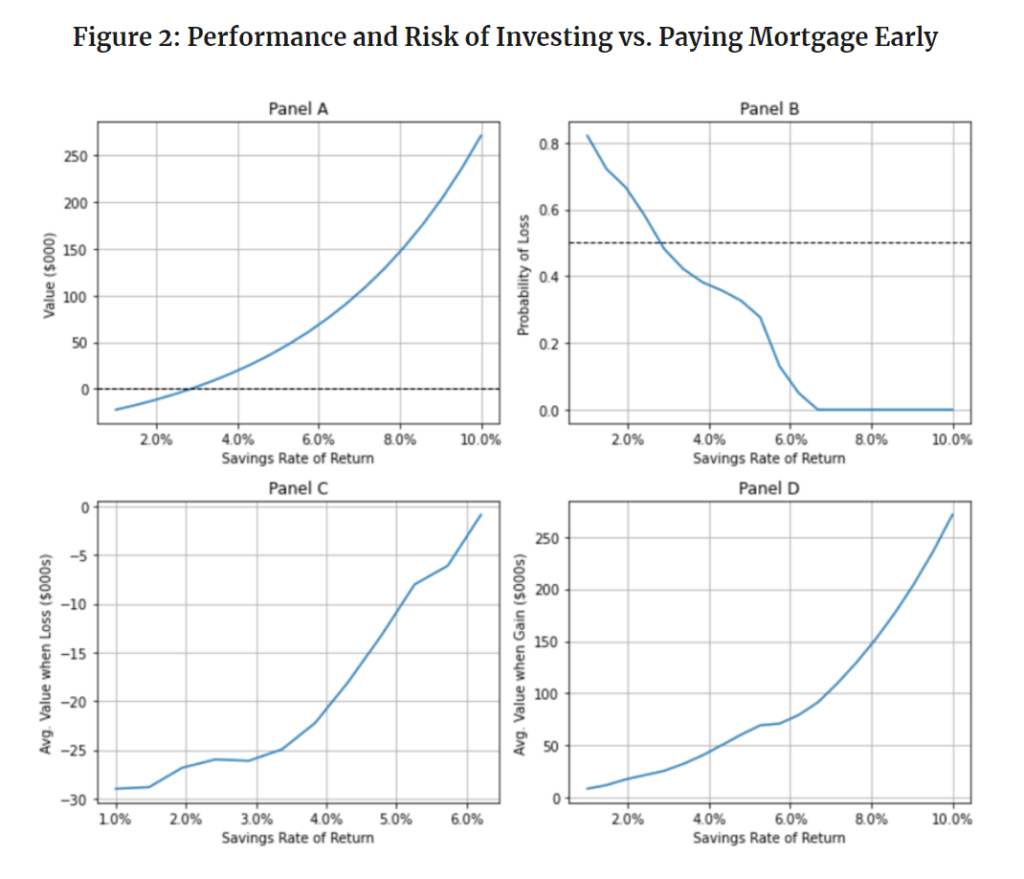

Panel A shows that as the return on Lena’s savings increases, i.e., we move from left to right along the horizontal axis, the value of investing the money relative to paying off the mortgage early increases. At a 3% savings return, the cost of her mortgage, Lena would be indifferent between saving extra money and paying down her mortgage early because both options lead to similar average savings balances after 30 years. Savings rates higher (lower) than 3% lead to higher (lower) savings for Lena if she invests her money as opposed to paying down her mortgage early. For example, a 5.5% average return on savings, half that of the historical return, leads to an extra $57,000 in after-tax savings if Lena invests the $210 per month as opposed to using it to pay down her mortgage more quickly.

Panel B illustrates the relative risk of the investment strategy. When the return on savings is 3%, the same as the cost of the mortgage, the choice between investing the money and paying down the mortgage comes down to a coin flip; there is a 50-50 chance that either option will lead to a better outcome. However, if future average market returns are 5.5%, for example, the probability that investing extra money leads to less savings than paying down the mortgage early is only 26%. For average returns above 6.5%, the probability that investing the extra money is a bad choice is zero. In other words, there hasn’t been a 30-year historical period in which the average stock market return was below 3%, even when the average return for the 100-year period was only 6.5%.

Author(s): Michael R. Roberts

Publication Date: 15 March 2021

Publication Site: Knowledge @ Wharton