HB 2451 addresses disparate pension benefits among Chicago firefighters. Currently, employees eligible for a pension in the Firemen’s Annuity and Benefit Fund of Chicago (FABF) who were born after January 1, 1966 are granted a 1.5 percent COLA. However, firefighters who may have started on the force the same day, may unfairly receive different benefits based on their dates of birth. The legislation addresses this discrepancy by adjusting the COLA for these firefighters from 1.5 percent to 3 percent.

The legislation eliminates the 30 percent cap on cumulative COLA adjustments. For employees eligible for a 1.5 percent COLA, they would have hit the cap at 20 years. The reforms made in this legislation provides firefighters the ability to plan for themselves and their families.

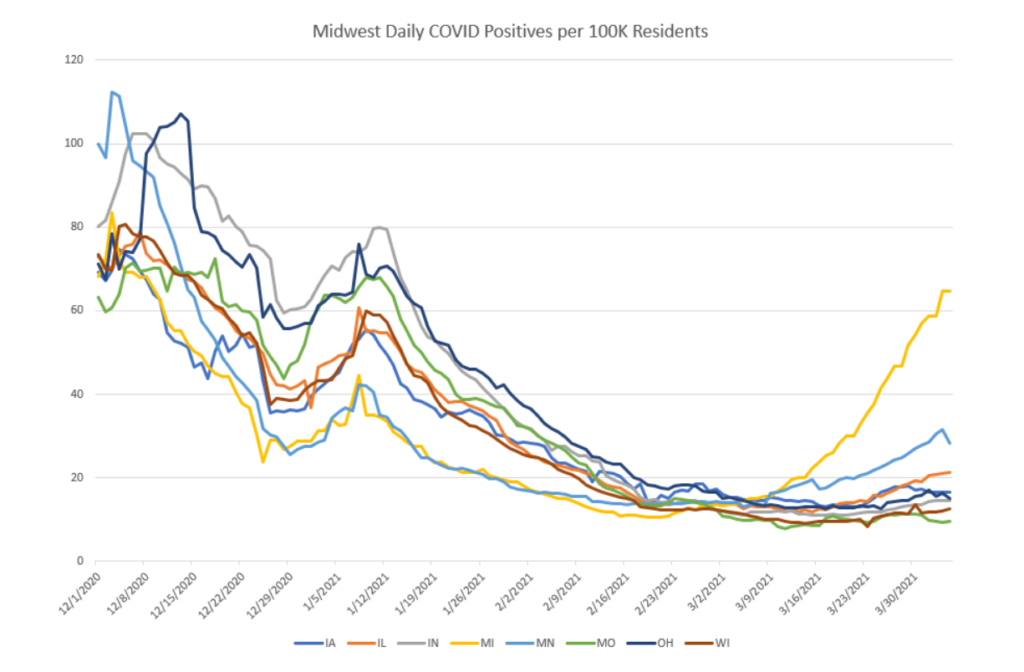

My current plan is to stop following COVID numbers after this coming May. But a lot of that plan rested on this assumption that, as we get really high up there with vaccine numbers, the COVID data would become less and less interesting as it just kind of fizzles out.

Michigan is currently putting that assumption to the test.

*takes deep breath*

The numbers out of Michigan have all the markings of a classic COVID surge. I could maybe make the case that it’s not as steep as we would have expected and maybe it will plateau in the next week or two, but I’ve been expecting that the rate of vaccinations would temper this kind of a surge.

Author(s): PoliMath

Publication Date: 6 April 2021

Publication Site: Marginally Compelling at Substack

SB 84’s legislative analysis estimates the proposed change would save the state $8.3 million in the first year, increasing to $109.7 million annually after 30 years.

As of June 30, FRS held $164.3 billion in assets against $200.3 billion in liabilities, leaving $36 billion in unfunded liabilities, which means the FRS could cover 82 percent of its obligations if every member retired today.

Templin said an 80-percent threshold is the “gold standard” in pension viability and the FRS is “in very good shape.”

Which makes it attractive for manipulation, said AFSCME Florida Retiree Executive Board member Maxie Hicks.

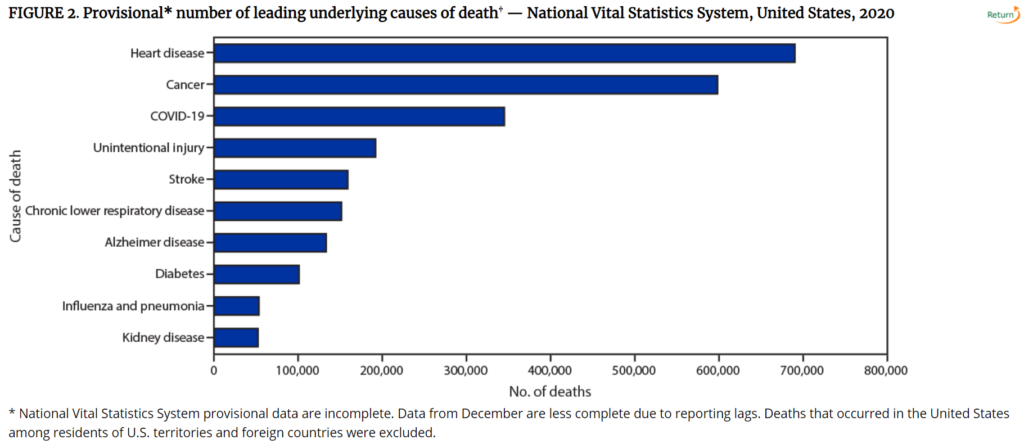

During January–December 2020, the estimated 2020 age-adjusted death rate increased for the first time since 2017, with an increase of 15.9% compared with 2019, from 715.2 to 828.7 deaths per 100,000 population. COVID-19 was the underlying or a contributing cause of 377,883 deaths (91.5 deaths per 100,000). COVID-19 death rates were highest among males, older adults, and AI/AN and Hispanic persons. The highest numbers of overall deaths and COVID-19 deaths occurred during April and December. COVID-19 was the third leading underlying cause of death in 2020, replacing suicide as one of the top 10 leading causes of death (6).

The findings in this report are subject to at least four limitations. First, data are provisional, and numbers and rates might change as additional information is received. Second, timeliness of death certificate submission can vary by jurisdiction. As a result, the national distribution of deaths might be affected by the distribution of deaths from jurisdictions reporting later, which might differ from those in the United States overall. Third, certain categories of race (i.e., AI/AN and Asian) and Hispanic ethnicity reported on death certificates might have been misclassified (7), possibly resulting in underestimates of death rates for some groups. Finally, the cause of death for certain persons might have been misclassified. Limited availability of testing for SARS-CoV-2, the virus that causes COVID-19, at the beginning of the COVID-19 pandemic might have resulted in an underestimation of COVID-19–associated deaths.

This report provides an overview of provisional U.S. mortality data for 2020. Provisional death estimates can give researchers and policymakers an early indication of shifts in mortality trends and provide actionable information sooner than the final mortality data that are released approximately 11 months after the end of the data year. These data can guide public health policies and interventions aimed at reducing numbers of deaths that are directly or indirectly associated with the COVID-19 pandemic and among persons most affected, including those who are older, male, or from disproportionately affected racial/ethnic minority groups.

Author(s): Farida B. Ahmad, Jodi A. Cisewski, Arialdi Miniño, Robert N. Anderson

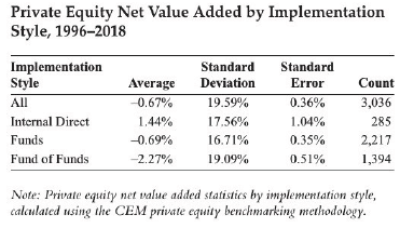

CEM, using a simple mix of small-cap indexes, found that even though private equity funds deliver what looks to be outsized raw returns, they fall short of CEM’s benchmark since 1996. However, as we’ve also said for some time, the big exception is investing in house, which CEM calls “internal direct”. And the worst, natch, is fund of funds, which have an extra layer of fees.

There are two additional reasons the CEM findings are deadly. First, the time period they look at, going back to 1996, includes a substantial portion of the 1994-1999 “glory years” where private equity firms were coming back from a period of disfavor after the late 1980s leveraged buyout crash. Less competition for deals meant better buying prices and better returns. Alan Greenspan dropping interest rates for a full nine quarters after the dot-com collapse was the first episode of the Fed driving money into high risk investment strategies by creating negative real returns for a sustained period, and the rush of money into private equity elevated deal prices.

PSERS is trying to depict the performance overstatement as an error but its body language says otherwise. It has launched an investigation of its three top staff members and has gone from denying that PSERS has any information that anything criminal had taken place to ducking the question.

The Inquirer described how three of PSERS’ 15 board members voted against a staff effort to say the return numbers were fine after some sort of not fully disclosed brouhaha with an outside consultant.

…..

The “impact on PSERS tax exempt status” is alarming, and it’s frustrating that the article does not probe what the issue might be.

Needless to say, expect more shoes to drop as the FBI keeps digging. A friend who was the DA for Bridgeport, the most corrupt city in Connecticut, said the FBI aren’t the brightest bulbs but are relentless and as a result generally take down their targets.

Week 1 Monday, May 10: (General) Actuarial Transformation: Trends & Insights across Data, Processes, Models, and People

Tuesday, May 11: (Life) Consolidated Appropriations Act, 2021: Changes to IRS code Section 7702 Wednesday, May 12: (General/Professionalism) Emerging Professionalism Issues in 2021 Thursday, May 13: (Investments) Macro Economic & Market Update

Thursday, May 13, 4pm EDT: (General) Networking Session Friday, May 14: (Health) The Role of Behavioral Health‐Now and in the Future

Week 2 Monday, May 17, 9am EDT: (General) Actuaries Working in International Landscape Tuesday, May 18: (Health) Health Technology, Consumerism and the Explosion of Telehealth Wednesday, May 19: (Pension) New Pension Relief under ARPA: Its Implications for Pension Plans Thursday, May 20: (Life/Annuities) Mortality Differential by Socioeconomic Categories in the US Friday, May 21: (Life/Annuities) Life Reinsurance 101 Panel Discussion

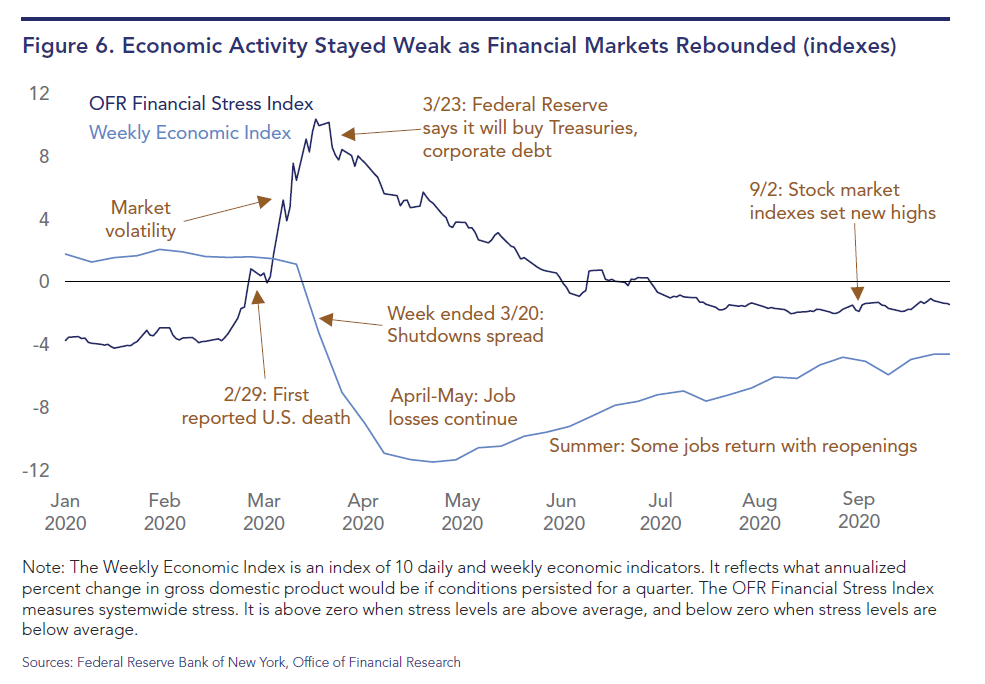

There remains a striking contrast between the quick recovery of financial markets and the slower recovery of the economy, which experienced the highest unemployment rate since World War II (see Figures 5 and 6). The possibility remains for heavy ongoing credit losses and failures. Consumer spending and business investment face pervasive uncertainty about the course of the pandemic and its consequences.

The phrase “coverage gap,” heard often from life insurance company executives, is defined as “the shortfall in the amount of life insurance cover necessary to maintain the current living standards of dependents.” Life insurance companies devote extraordinary amounts of time, effort, and expense trying to educate underinsured individuals about the need to protect themselves and their families from this gap by buying more cover. Could our industry not be addressing one of the key issues leading to the lack of consumer enthusiasm for our products?

Here’s the issue: insurance products and contracts are not consumer-friendly. To the average person, life and living benefits products are at least as byzantine as Brazil’s political system, and the language of insurance contracts could almost be considered an actual dialect. Insurance is thus fertile ground for the manifestation of rational ignorance among potential customers, who are already known to be more likely to pay attention to information about it if it comes from friends and social media posts. (I pity the buyer researching concepts and options such as pure protection, accumulation, critical illness, disability income, or long-term care.)

Author(s): Ronald Poon-Affat

Publication Date: March 2021

Publication Site: Reinsurance News at the Society of Actuaries

Given these advances in understanding the theoretical methods of evaluating multiple, related mortality data sets, it is particularly promising that the Human Mortality Database, with the SOA’s sponsorship, has recently made available mortality data for the United States at the level of the individual county. Moreover, Professor Magali Barbieri of University of California, Berkeley in January 2021 published an SOA Research Report[3] on “Mortality by Socio-economic Category in the United States” using this data series. Professor Barbieri is one of the directors of the HMD project, which is jointly run by UC Berkeley and the Max Planck Institute for Demographic Research in Rostock, Germany and support from the Center on the Economics and Development of Aging (CEDA) and the French Institute for Demographic Studies (INED). In her paper, Barbieri studies socio-economic differences linked to mortality differentials by county, based on information available at the county level regarding education, occupation, employment, income, and housing. The gap between the highest and lowest county decile is huge and growing. In 2018, the qx-rate for 45-year-old men in counties with the lowest Socioeconomic Index Score (SIS) was 2.5 times that for men of that age in counties with the highest SIS. This gap is even greater than the difference between smokers and non-smokers. Professor Barbieri’s report shows the widening trend between the different socio-economic strata which she captures by grouping the counties into deciles by SIS. While the highest SIS score is associated with a life expectancy that matches or even beats the OECD average, people living in counties with the lowest SIS have hardly seen any improvement in their life expectancy over the last four decades. Comparing the average life expectancy at birth within the highest decile of counties to the lowest, there was a gap of 3.0 years in 1982, the first year for which consistent data was available. This gap has more than doubled since then, rolling in at 6.6 years difference in life expectancy in 2018. That is an increase of 120 percent. Worse still, the gender gap once again manifests itself in the mortality trends, with females showing an increase of the socio-economic mortality gap of 260 percent over the 36-year period, compared to 76 percent for males.

Author(s): Kai Kaufhold

Publication Date: March 2021

Publication Site: Reinsurance News at the Society of Actuaries

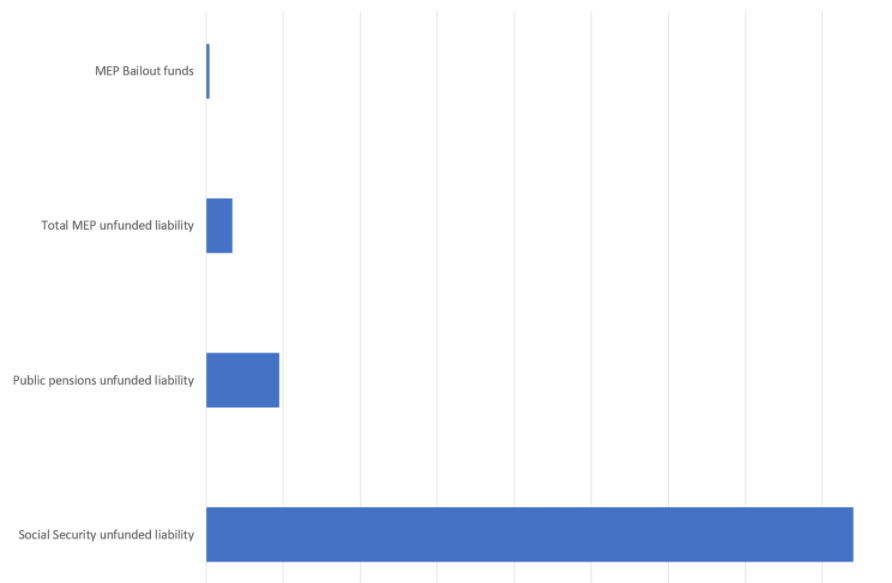

There may eventually be MEP reforms, but with a big cash injection into Central States Teamsters, the reckoning day has been pushed off.

The real crisis was Central States Teamsters going under. It would have taken down the PBGC. The puny plans like Warehouse Employees Union Local No. 730 Pension Trust (total liability amount: $474,757,777) are drops in the bucket compared with Central States (total liability amount: $56,790,308,499).