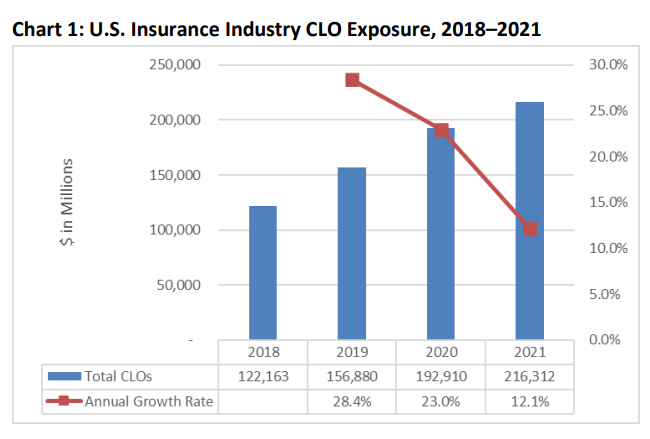

U.S. insurers’ exposure to CLOs increased significantly over the last few years, as they have represented an attractive alternative investment with higher yields than traditional investments. As of year-end 2021, U.S. insurers’ exposure to CLOs collateralized predominantly by leveraged bank loans and middle market loans increased by 12% to $216.3 billion in BACV from $192.9 billion at year-end 2020 and $156.9 billion at year-end 2019 (see Chart 1). However, the pace of growth has slowed from 23% and 28% at year-end 2020 and year-end 2019, respectively.

Author(s): Jennifer Johnson, Michele Wong, Jean-Baptiste Carelus

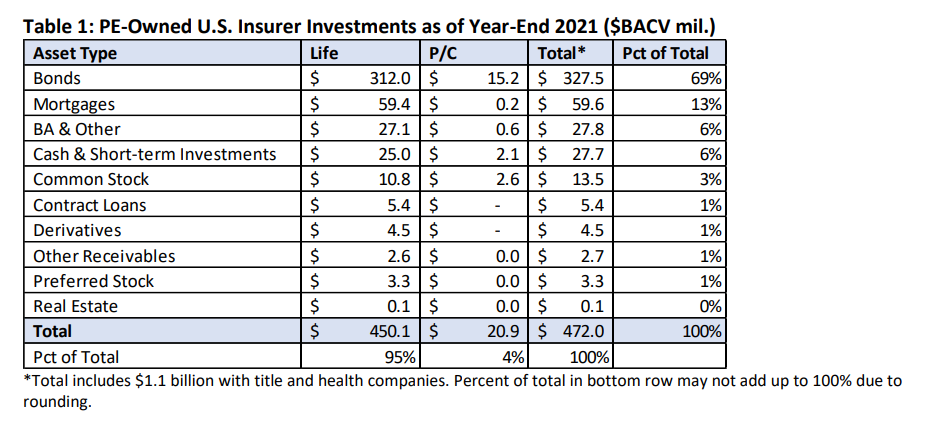

The BACV of total cash and invested assets for PE-owned insurers was about 6% of the U.S. insurance industry’s $8.0 trillion at year-end 2021, down slightly from 6.5% of total cash and invested assets at year-end 2020. The number of PE-owned insurers, however, increased to 132 in 2021 from 117 in 2020, but they were about 3% of the total number of legal entity insurers at both year-end 2021 and year-end 2020.

Consistent with prior years, U.S. insurers have been identified as PE-owned via a manual process. That is, the NAIC Capital Markets Bureau identifies PE-owned insurers to be those who reported any percentage of ownership by a PE firm in Schedule Y, and other means of identification such as using third-party sources, including directly from state regulators. As such, the number of U.S. insurers that are PE-owned continues to evolve.1 Life companies continue to account for a significant proportion of PE-owned insurer investments at year-end 2021, at 95% of total cash and invested assets (see Table 1). This represents a small decrease from 97% at year-end 2020 (see Table 2). Notwithstanding, there was a slight increase in PE-owned insurer investments for property/casualty (P/C) companies, to 4% at year-end 2021, compared to 3% the prior year. In addition, there was also a small increase in total BACV for PE-owned title and health companies’ investments, at about $1.1 billion at year-end 2021, compared to under $1 billion at yearend 2020.

Author(s): Jennifer Johnson and Jean-Baptiste Carelus

Publication Date: 19 Sept 2022

Publication Site: NAIC Special Capital Markets Reports

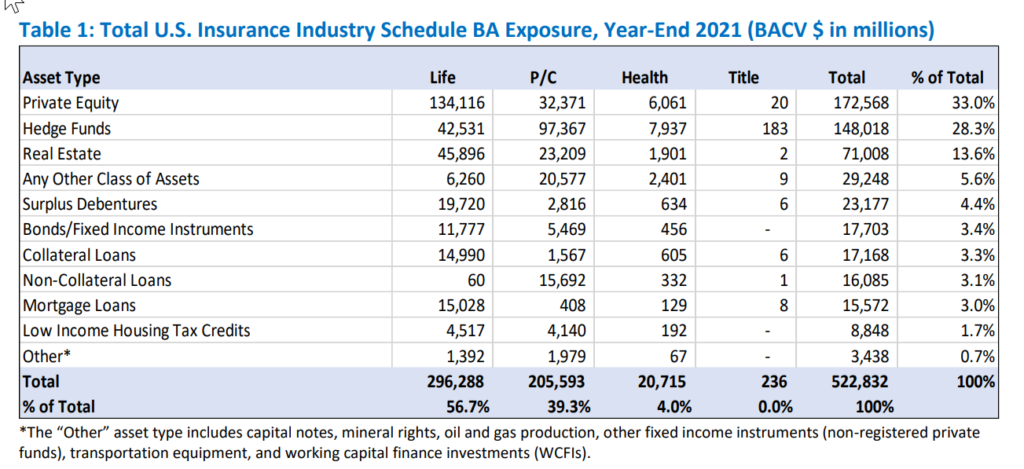

The U.S. insurance industry’s reported BACV of $522.8 billion in other long-term invested assets on Schedule BA represented an increase of 14.8% at year-end 2021 compared to year-end 2020 (see Table 1 and Table 2). Schedule BA assets have experienced strong double-digit growth in recent years, with 2021’s 15% increase in exposure following YOY growth of 13% and 10% in 2020 and 2019, respectively. Total Schedule BA exposure as of year-end 2021 represented 6.5% of the industry’s total cash and invested assets, an increase from 6.1% as of year-end 2020 and 5% as of year-end 2012.

Like previous years, hedge fund, private equity, and real estate investments represented most of the industry’s Schedule BA exposure. Together, they accounted for 75% of total exposure at year-end 2021 compared to 70% at year-end 2020. Exposure to private equity investments experienced significant growth, increasing by 34% YOY to $173 billion as of year-end 2021. Private equity’s share of total Schedule BA exposure rose to 33% from 28% at year-end 2020, surpassing hedge fund investments to become the largest component of the industry’s exposure.

Author(s): Michele Wong and Jean-Baptiste Carelus

Publication Date: 3 June 2022

Publication Site: NAIC Capital Markets Special Report

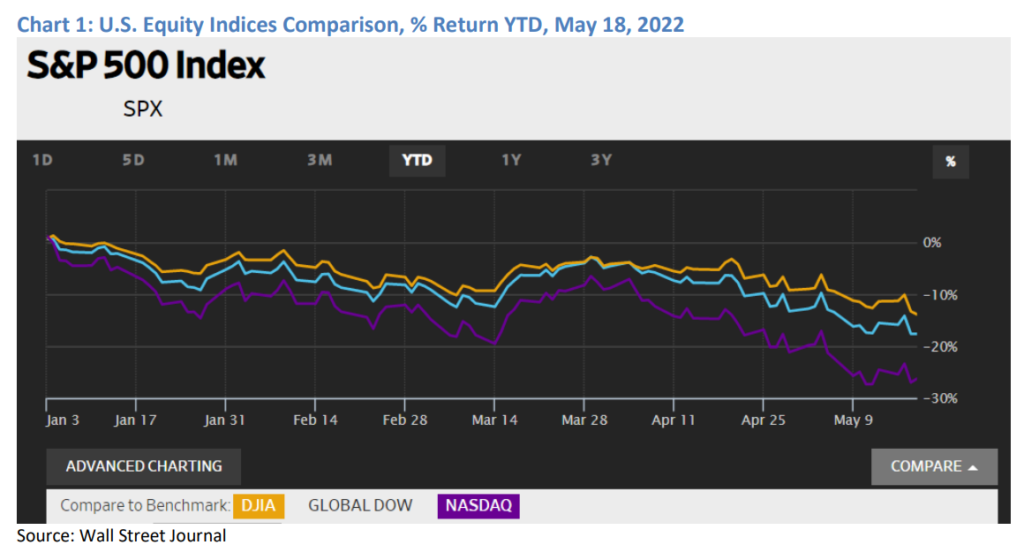

On May 19, the S&P 500 opened the day near bear market territory; i.e., at a 20% drop from a recent high. On May 18, the S&P 500 experienced a 4% decline—the largest single-day decrease since June 2020. The last time the S&P 500 entered bear market territory was in March 2020, albeit short-lived, as the market turned around and headed into a two-year rally that peaked in early January 2022.

The current equity market losses (and some corporate bond losses) are primarily the result of several factors: 1) earnings reports from large American retailers, including Walmart and Target, show evidence that the continued high inflation rate may be affecting consumer demand; 2) the war in Ukraine has added to inflationary pressures, prompting the Federal Reserve (Fed) to increase interest rates and reduce bond holdings; and 3) recent COVID-19 shutdowns in China have led to a slowdown in the world’s second largest economy.

Author(s): Jennifer Johnson and Michele Wong

Publication Date: 19 May 2022

Publication Site: NAIC Capital Markets Special Report

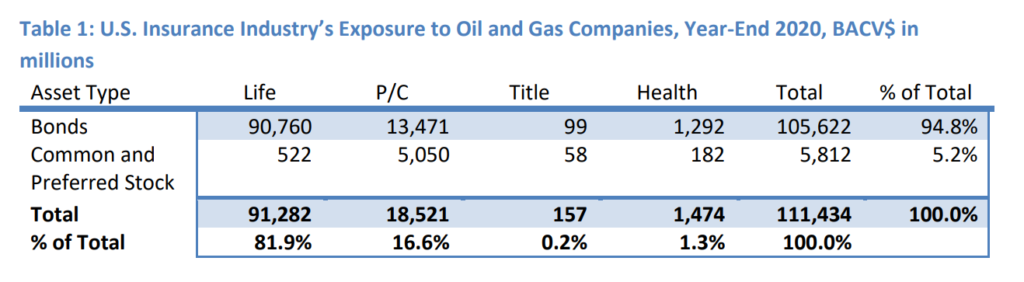

Table 1 identifies the year-end 2020 bond, common stock and preferred stock exposure of the U.S. insurance industry to oil and gas companies. The industry’s $111 billion book/adjusted carrying value (BACV) exposure represented approximately 1.5% of the industry’s total cash and invested assets as of year-end 2020. Oil and gas companies will benefit from the rise in oil prices, and they are currently in a much better financial position than during 2020 when Brent crude prices briefly fell below $10 per barrel and remained depressed relative to historical levels due to lower demand resulting from the effects of the COVID-19 pandemic.

Author(s): Michele Wong, Jennifer Johnson and Jean-Baptiste Carelus

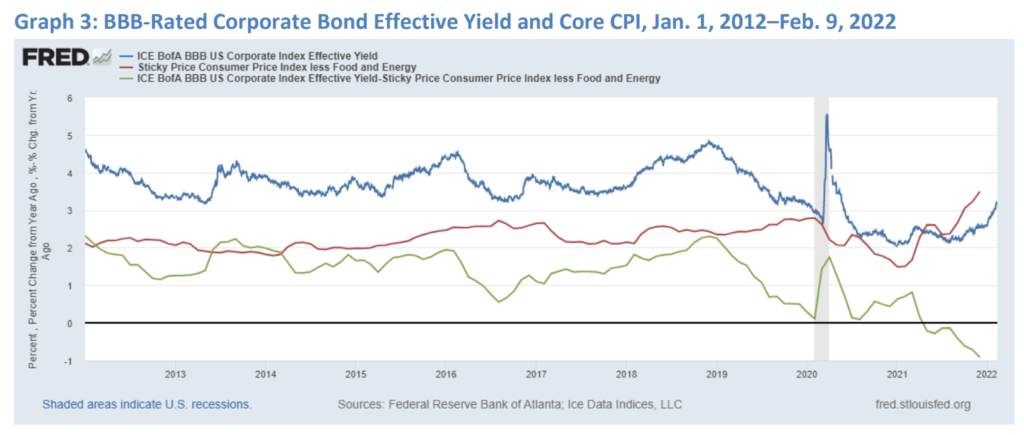

While U.S. insurance companies have adapted to investing in a world of low interest rates, they are now also facing the challenge of investing in a high inflationary environment whereby yields may not be providing adequate returns on investment on an inflation-adjusted basis. Using a similar approach to estimating real interest rates in Chart 1, we estimate how corporate bond yields are holding up against high inflation

….

Graph 3 shows similar data for BBB-rated corporate bonds. With BBB yields generally higher than A yields, the difference between the two measures has been negative for a shorter period of time. Real yields did not turn negative until May 2021, and they dipped to almost -1% in December 2021.

Author(s): Michele Wong and Jennifer Johnson

Publication Date: 15 Feb 2022

Publication Site: NAIC Capital Markets Bureau Hot Spot