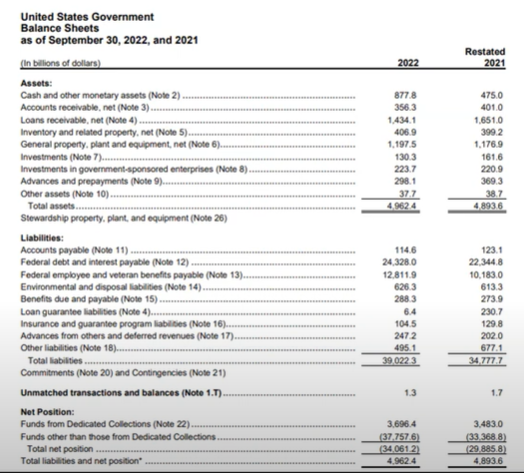

I got a great question from a finance student today, asking whether the “pecking order” theory of corporate capital structure could be applied to the government. OK, let’s think this out. Who comes first, in the pecking order?

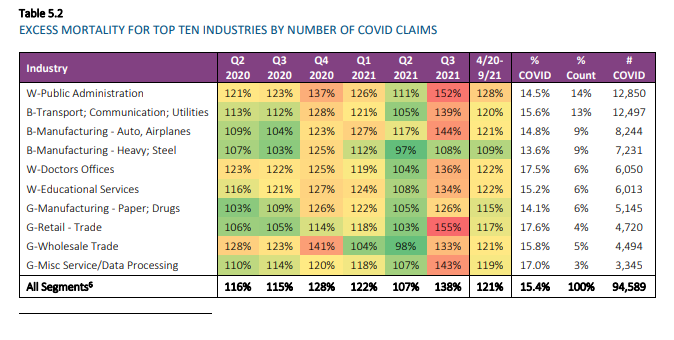

Table 5.2 shows more detailed industry results for the top ten industry segments by number of COVID claims. Most of these industries were in the top ten for the July 2021 report as well. As we now have more quarters with more complete results, both the A/E ratios for April 2020 through September 2021, as well as the COVID claims as a percentage of baseline claims, showed greater consistency across industries than in the previous report. Public Administration continues to be a key driver of high A/E ratios for the White Collar category. Doctors (Healthcare, also White Collar), Retail Trade (Grey Collar), and Misc. Services (Grey Collar) have the highest COVID claims as a percentage of baseline claims. Heavy Steel Manufacturing (Blue Collar) has a much lower A/E ratio than the other top 10 industries. In the table below, “B,” “W,” and “G” refer to Blue Collar, White Collar, and Grey Collar, respectively.

It should be noted that the high A/E ratios for Public Administration are driven by experience in the Executive, Legislative, and General Government segment (Standard Industry Classification [SIC] codes 9100-9199). This segment does not include police and fire and represents over 85% of claims in the broader Public Administration segment.

Video:

Publication Date: January 2022

Publication Site: Society of Actuaries Research Institute

OpenAI inside Excel? How can you use an API key to connect to an AI model from Excel? This video shows you how. You can download the files from the GitHub link above. Wouldn’t it be great to have a search box in Excel you can use to ask any question? Like to create dummy data, create a formula or ask about the cast of the The Sopranos. And then artificial intelligence provides the information directly in Excel – without any copy and pasting! In this video you’ll learn how to setup an API connection from Microsoft Excel to Open AI’s ChatGPT (GPT-3) by using Office Scripts. As a bonus I’ll show you how you can parse the result if the answer from GPT-3 is in more than 1 line. This makes it easier to use the information in Excel.

The private market for flood insurance in the United States measures approximately $300 million in annual premium. This is less than 10 percent of the $3.7 billion in flood insurance premium written by the federal government’s National Flood Insurance Program (NFIP). Private insurers offering flood insurance are not operating on the same playing field because many NFIP policies are subsidized and underpriced. The creativity of private insurers, guided by the dynamics of a free and competitive market, will eventually drive out inefficiency and false price signals, and make available to homeowners and businesses the flood insurance they need at the right cost.

We invite you to an online discussion examining the obstacles and opportunities for private insurers featuring flood insurance entrepreneur Trevor Burgess, and R Street’s Jerry Theodorou and Caroline Melear.

Author(s): Jerry Theodorou, Trevor Burgess, Caroline Melear

In a groundbreaking TED-style talk, Dominic Lee, ACAS takes the audience on a multisensory journey beyond the boundaries of traditional insurance. He presents a framework for the actuarial profession to step into the future and claim its rightful place as a dominant force in the world of risk: Reimagine, Embrace and Explore.

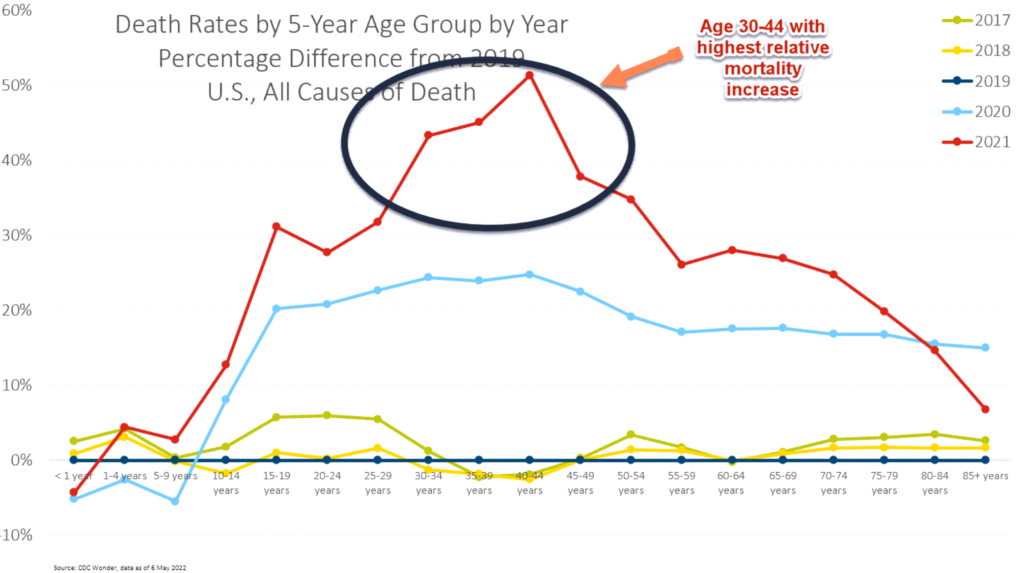

For 2021, the worst relative increase in mortality, compared to 2019, was for ages 30-44.

[I have called it the Millennial Massacre, but it obviously overlaps with Gen X…. and Middle Age Massacre doesn’t exactly work, either. Dang the allure of alliteration].

We will see in a moment that most of that mortality increase didn’t come from COVID.

If you look at overall mortality, obviously total mortality for this age group is much lower than for those much older.

A 5% increase in mortality for those aged 85+ will translate to a much larger number of deaths, but a 50% increase in mortality for those aged 40-44 is extremely worrisome to actuaries and insurers even if the absolute number of deaths is lower in impact. We’re setting reserves and expectations based on certain assumptions, and we’re generally not assuming fluctuations of 50% — that’s just nuts compared to our historical experience…..

The insurance industry is unique in that the cost of its products—insurance policies—is unknown at the time of sale. Insurers calculate the price of their policies with “risk-based rating,” wherein risk factors known to be correlated with the probability of future loss are incorporated into premium calculations. One of these risk factors employed in the rating process for personal automobile and homeowner’s insurance is a credit-based insurance score.

Credit-based insurance scores draw on some elements of the insurance buyer’s credit history. Actuaries have found this score to be strongly correlated with the potential for an insurance claim. The use of credit-based insurance scores by insurers has generated controversy, as some consumer organizations claim incorporating such scores into rating models is inherently discriminatory. R Street’s webinar explores the facts and the history of this issue with two of the most knowledgeable experts on the topic.

Featuring:

[Moderator] Jerry Theodorou, Director, Finance, Insurance & Trade Program, R Street Institute Roosevelt Mosley, Principal and Consulting Actuary, Pinnacle Actuarial Services Mory Katz, Legacy Practice Leader, BMS Group

R Street Institute is a nonprofit, nonpartisan, public policy research organization. Our mission is to engage in policy research and outreach to promote free markets and limited, effective government.

We believe free markets work better than the alternatives. We also recognize that the legislative process calls for practical responses to current problems. To that end, our motto is “Free markets. Real solutions.”

We offer research and analysis that advance the goals of a more market-oriented society and an effective, efficient government, with the full realization that progress on the ground tends to be made one inch at a time. In other words, we look for free-market victories on the margin.

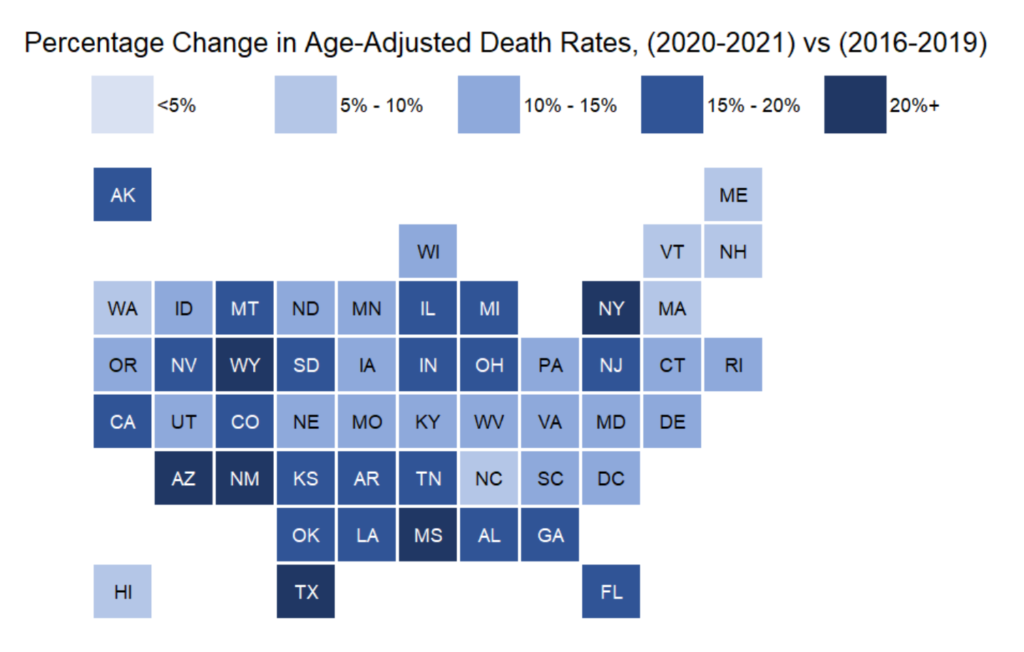

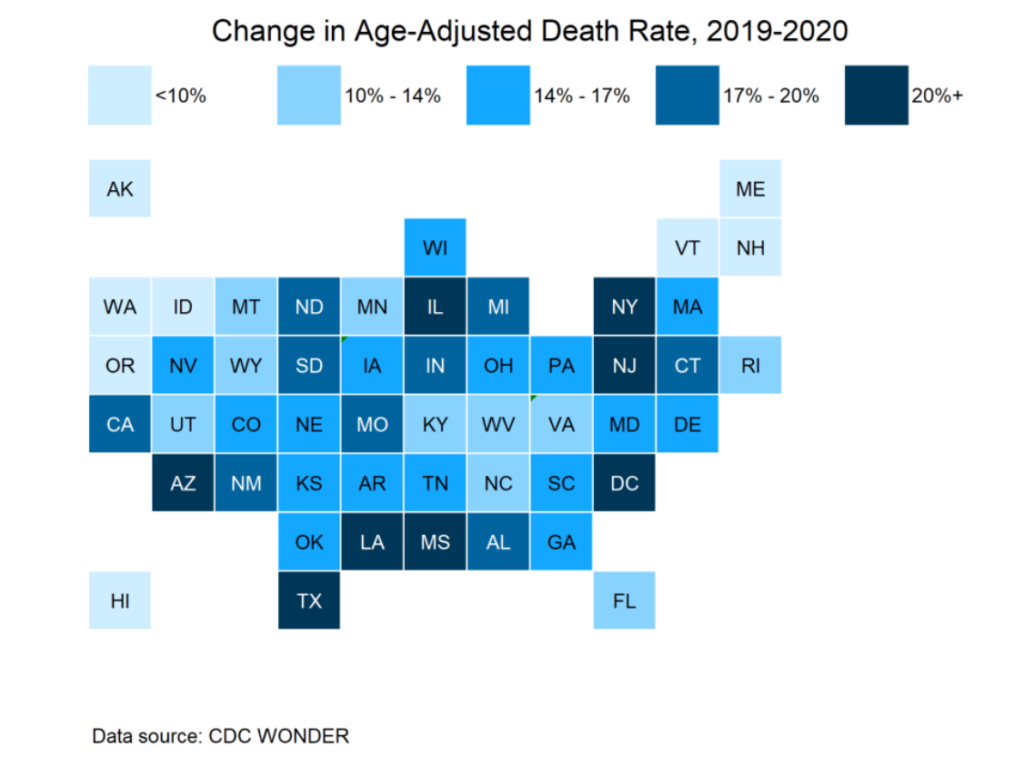

With this tile grid map, we can see that the two-year mortality experience has been horrible, even on an age-adjusted basis. I will be using age-adjusted death rates [using the standard 2000-reference-age-adjustment] for all the comparisons. The methodology is at the end of the post.

I warn against taking any meaning from North Carolina, as it has a data-reporting problem. Hawaii, however, really does have a low increase in mortality, and I believe it is credible that the mortality increase of the northeast is also low. I am not sure how credibly to take the increase in mortality of Wyoming, given its relatively small population.

However, we can see some patterns. In general, one has a “hot spot”, and then the increase falls off as you retreat from that peak. The large pattern is the high increase along the southern border — Arizona, New Mexico, Texas, Mississippi — and then the next layer above is less bad, and so forth. There is the Wyoming peak, falls off around there. There is the midwest cluster – Illinois, Michigan, Indiana, Ohio. And then New York/New Jersey.

As well we know, the excess mortality is driven primarily by COVID, which I will get to in the next major section, but let me share some ranking tables.

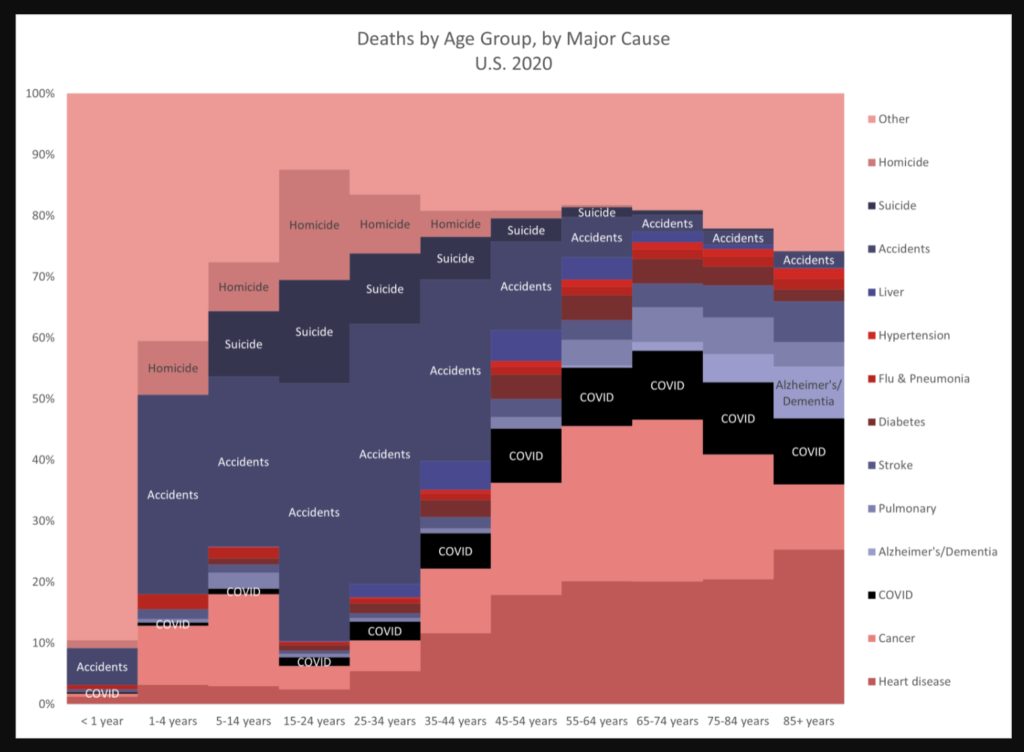

I highlighted a few of the cause-of-death trends. In particular, COVID (which, obviously, is biased more towards the old), and external causes of death: homicide, suicide, and accidents (which includes drug overdoses and motor vehicle accidents).

There are basically too many things going on in this graph, so there aren’t a lot of good choices for either me or the SOA. What I did was to pick four of the data series to highlight with data labels, as noted above (and I also slapped one data label on dementia for the oldest age group, just because). I am in the middle of a series going through how that external causes of death changed in 2020 — in particular, accidents and homicides went up, and really affected mortality for adults under age 45, plus male teens.

Yeah, check out heart disease and cancer (bottom of the graph). Ain’t old age great?

Actuarial News is a website Stu created for me to use as a place to collect all the articles, websites, data sources, etc. that I like to use for my research and writing. I tend to develop ideas over long periods, and I prefer my selections over trying to use regular search.

As noted in the video, I used to use the old Actuarial Outpost (RIP) as a repository for my articles on public pensions and finance, but now I use Actuarial.News.

By the way, for any readers seeking actuarial discussion as once was provided by the old Outpost, check out goActuary. I have a thread on spreadsheet screwups and one on non-pandemic mortality, for instance.

The ranking tables do reflect where COVID hit hard in 2020 — the spring 2020 wave in the northeast, and the summer 2020 wave along the south and southwest (Texas, in particular). No, Florida didn’t show its big COVID impact until January 2021, so it’s pretty far down on this ranking table.

This way, we can see if there are any geographic patterns. We did know the hot spots of NY, NJ, IL (mainly around Chicago), DC, TX, Louisiana (around New Orleans), Arizona. I had not been aware of Mississippi being so bad, but maybe that was spillover from New Orleans.