Link:https://content.naic.org/sites/default/files/capital-markets-hotspot-Equity-Market-Drop-Jan-2022.pdf

Graphic:

Excerpt:

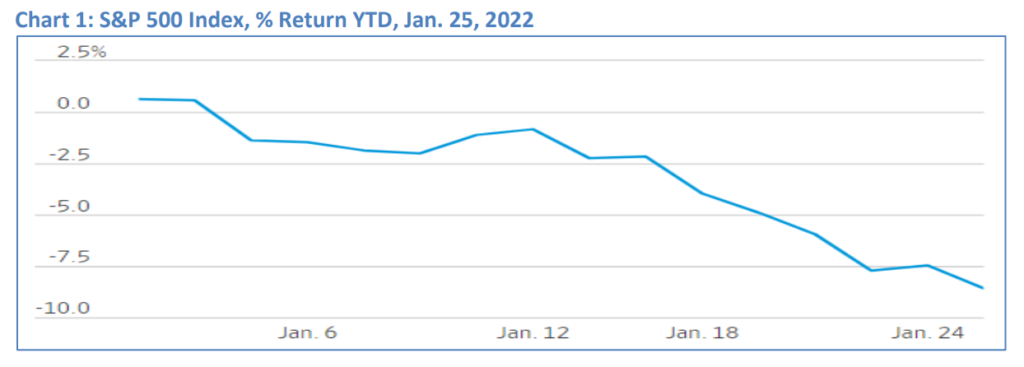

Both economic and geopolitical factors have caused some volatility in the financial markets, including a

recent significant decline in equity markets into “correction territory,” or a decrease greater than 10%.

Equity markets have been declining over the last few weeks after reaching a record high at the

beginning of 2022 when Standard & Poor’s 500 Index (S&P 500) reached almost 4,800. On Jan. 24, the

S&P 500 was down as much as 2% intraday, but it rebounded to finish the day up 0.3%. Volatility

continued into the following trading day, with the index declining 1.2% on Jan. 25.

Author(s): Jennifer Johnson, Michele Wong, and Jean-Baptiste Carelus

Publication Date:25 Jan 2022

Publication Site: NAIC Capital Markets Bureau