Graphic:

Excerpt:

The U.S. economy has made a solid recovery as COVID-19 vaccinations were made increasingly

available, social distancing began to ease, and businesses gradually reopened.

The International Monetary Fund (IMF), among other forecasters, expects the U.S. economy to

grow by about 6% in 2021, after contracting about 3.4% in 2020.

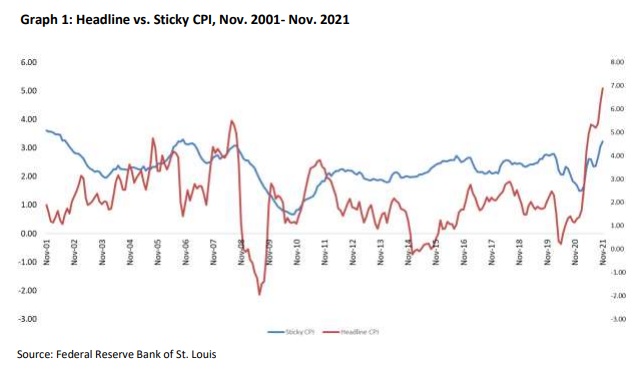

• Inflation reached a 39-year high of 6.8% in November following a strong rebound from the COVID19-induced recession.

• The ‘stronger for longer’ inflation rates prompted the Federal Reserve to accelerate the tapering

of its asset purchases and to suggest the likelihood of three rate hikes in 2022.

• The 10-year U.S. government bond yield has generally ranged between 1.3% and 1.7% in 2021,

increasing from less than 1% in 2020, due in part to fiscal stimulus aiding in economic recovery.

• Credit spreads have been muted in 2021 given robust global economic growth, favorable funding

conditions, and overall solid corporate performance despite higher costs and supply disruptions.

• Global stocks have achieved relatively high returns; in the U.S., the Standard & Poor’s (S&P) 500

posted seven record closing highs in November alone.

• The price of oil reached a seven-year high of $85 per barrel in 2021 as demand for oil normalized

while the global supply market tightened.

Author(s): : Jennifer Johnson and Michele Wong

Publication Date: 22 Dec 2021

Publication Site: NAIC Capital Markets Bureau Special Reports