Graphic:

Excerpt:

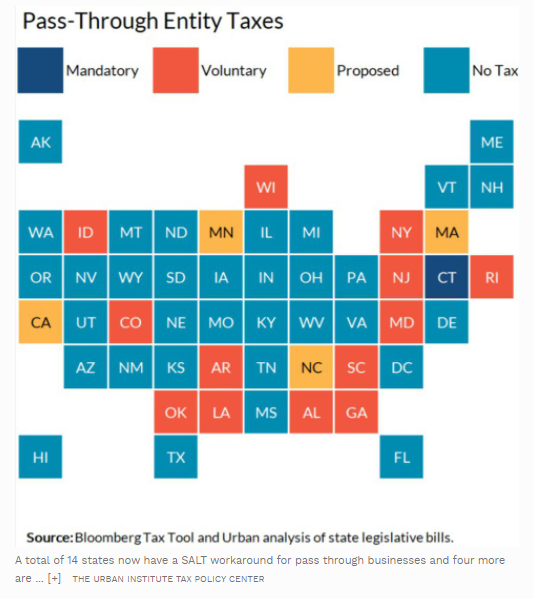

But PTE taxes create inequities based on type of income. For example, because these states now favor pass-through income over wages, a partner in a law firm can be effectively exempt from the SALT cap while an executive assistant or associate in the same firm remains subject to the deduction limitation. A doctor who is an employee of a corporation is barred from fully deducting state and local income taxes while a partner in a medical practice making the same income is exempt from the federal cap for these taxes.

Because the rules differ across states, businesses need to consider where partners live and where business income is generated. For example, non-resident partners might not benefit from the credits in their home state. Like New York, some states of residence allow credits against the taxes these partners owe from other states. But that isn’t always the case.

Keep in mind that these PTE taxes may be just a temporary fix. Congress may consider changes to the SALT cap in coming legislation. And the cap, along with all other individual tax changes in the TCJA, is scheduled to expire at the end of 2025.

Author(s): Kim S. Rueben

Publication Date: 24 June 2021

Publication Site: TaxVox at Tax Policy Center