Link:https://www.federalreserve.gov/publications/files/financial-stability-report-20211108.pdf

Graphic:

Excerpt:

Our view of the current level of vulnerabilities is as follows:

Asset valuations. Prices of risky assets generally increased since the previous report, and,

in some markets, prices are high compared with expected cash flows. House prices have

increased rapidly since May, continuing to outstrip increases in rent. Nevertheless, despite

rising housing valuations, little evidence exists of deteriorating credit standards or highly

leveraged investment activity in the housing market. Asset prices remain vulnerable to

significant declines should investor risk sentiment deteriorate, progress on containing the

virus disappoint, or the economic recovery stall.Borrowing by businesses and households. Key measures of vulnerability from business

debt, including debt-to-GDP, gross leverage, and interest coverage ratios, have largely

returned to pre-pandemic levels. Business balance sheets have benefited from continued

earnings growth, low interest rates, and government support. However, the rise of the

Delta variant appears to have slowed improvements in the outlook for small businesses.

Key measures of household vulnerability have also largely returned to pre-pandemic

levels. Household balance sheets have benefited from, among other factors, extensions

in borrower relief programs, federal stimulus, and high aggregate personal savings rates.

Nonetheless, the expiration of government support programs and uncertainty over the

course of the pandemic may still pose significant risks to households.Leverage in the financial sector. Bank profits have been strong this year, and capital

ratios remained well in excess of regulatory requirements. Some challenging conditions

remain due to compressed net interest margins and loans in the sectors most affected

by the COVID-19 pandemic. Leverage at broker-dealers was low. Leverage continued

to be high by historical standards at life insurance companies, and hedge fund leverage

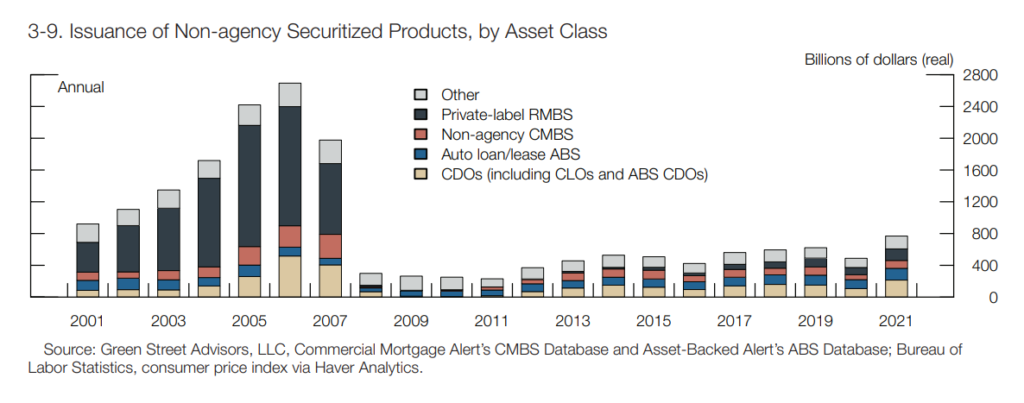

remained somewhat above its historical average. Issuance of collateralized loan obligations (CLOs) and asset-backed securities (ABS) has been robust.Funding risk. Domestic banks relied only modestly on short-term wholesale funding and

continued to maintain sizable holdings of high-quality liquid assets (HQLA). By contrast,

structural vulnerabilities persist in some types of MMFs and other cash-management

vehicles as well as in bond and bank loan mutual funds. There are also funding-risk vulnerabilities in the growing stablecoin sector.

Publication Date: November 2021

Publication Site: Federal Reserve