Link: https://www.governing.com/finance/the-fed-is-normalizing-heres-what-public-financiers-need-to-know

Graphic:

Excerpt:

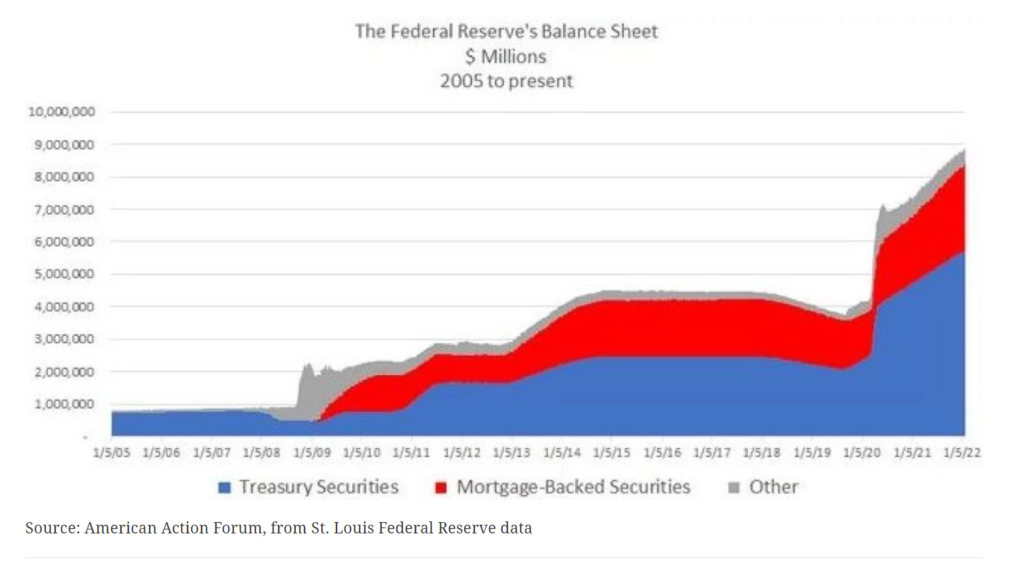

Of the $8.3 trillion of liquid marketable securities in the Fed’s portfolio (see the chart below), 37 percent are overnight repos and Treasury securities maturing in one year or less, 26 percent are T-notes maturing in one to five years, and another 30 percent are mortgage-backed securities issued by Fannie Mae and Freddie Mac, which pay down principal and interest monthly. So all it takes to pull back the excessive monetary stimulus left over from the COVID-relief era is to let such holdings roll off in 2022-24 without replacing them with new purchases. Operationally, it’s really not rocket science — it’s just a matter of conviction and messaging. Unlike the rising stairstep expected in the Fed’s overnight rates, its bond portfolio runoff won’t make nightly news headlines; it’s like watching paint dry. In this regard, doing nothing is actually doing something quite constructive on the inflation front, despite the lack of fanfare.

What would be the impact on interest rates? Little doubt they must go higher, barring an exogenous shock like a global virus lockdown or a Ukraine-war flight-to-safety. The key question is really how much higher, and how fast. My best guess is that markets have recently discounted about one-third of the potential move higher in long-term rates.

Author(s): Girard Miller

Publication Date: 15 Feb 2022

Publication Site: Governing