Graphic:

Excerpt:

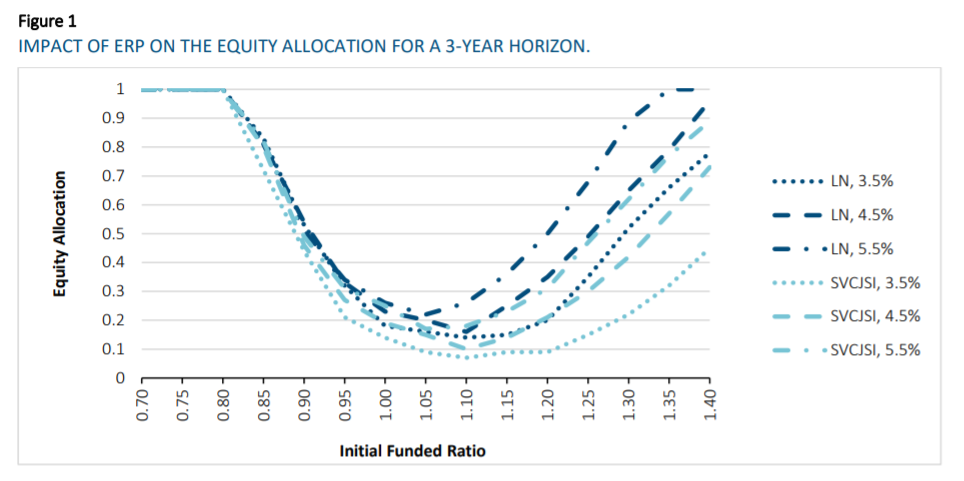

In this essay, we consider an additional application. Using the utility framework described by Warren (2019), we

examine the impact of using one of BB’s fitted jump-diffusion models on a pension plan sponsor’s long-term asset

allocation decision. We want to compare asset allocation results to those using the standard finance workhorse

model of a geometric Brownian motion (i.e., lognormal return generating process or LN hereafter).

Author(s):

Jean-François Bégin, PhD, FSA, FCIA

Mathieu Boudreault, PhD, FSA, FCIA

David R. Cantor, CFA, FRM, ASA

Kailan Shang, FSA, ACIA, CFA, PRM

Publication Date: September 2021

Publication Site: Society of Actuaries