Link:https://taxfoundation.org/massachusetts-gross-receipts-tax/

Graphic:

Excerpt:

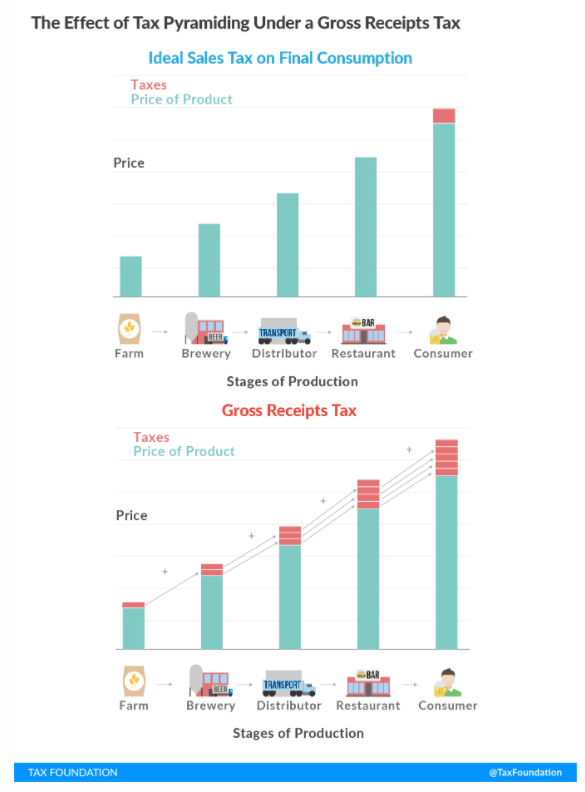

The economic harms of the gross receipts tax (GRT) were well understood by the early 20th century. Not only is the tax inequitable, but it is also inefficient and distortionary. That is why most states abandoned GRTs in the early 1900s, as states developed the capacity to administer less harmful taxes. Unfortunately, some policymakers in Massachusetts want to turn back the clock.

Today, only a handful of states levy any variation of the GRT. Those that still rely on them as a significant source of revenue (like Texas, Nevada, Ohio, and Washington) typically do so in lieu of one or more alternative taxes. None of these states imposes a corporate income tax, and Ohio repealed several other business taxes as well when it adopted its GRT.

Some Massachusetts policymakers, however, want to layer a GRT atop the state’s existing corporate income tax. If H.2855 becomes law, it would reduce the competitiveness of the Bay State and increase prices for consumers on already expensive goods and services. To make matters worse, Bay Staters would be asked to shoulder the added tax burden at a time when inflation is already eroding purchasing power at a rate not seen 1982.

Author(s): Timothy Vermeer

Publication Date: 9 Feb 2022

Publication Site: Tax Foundation